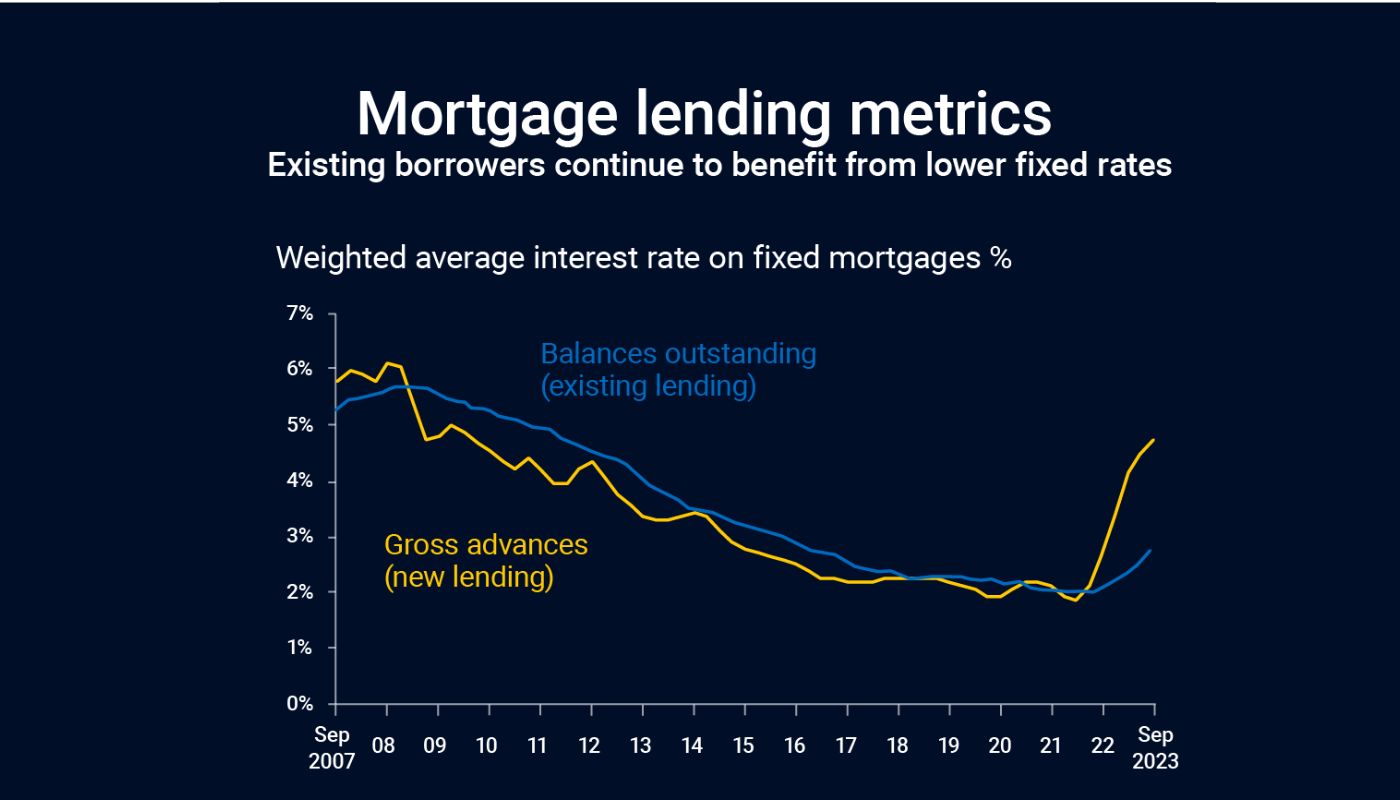

There is light at the end of the tunnel with these dreaded mortgage rates. The rates have dropped which buyers are now taking advantage of after much hesitation last year. However, it may be bad news for existing homeowners with mortgages coming to an end. As you can see from the graph below, the gap between homeowner’s existing mortgage rates and the latest mortgage rates is quite large which for many people, means a much larger monthly mortgage payment.

If you are about to come to the end of your mortgage product in the next 6 months, we highly recommend you start making preparations and considerations now. Don’t leave it till the last minute.

If you need some advice, let us know, we’re happy to come and see you free of charge.

Hopefully, this summary will help you understand what is good and what is bad about the mortgage rates at the moment…

The Bad News

- Mortgage borrowers on fixed rates have already escaped the worst of the interest rate rises and the direction of travel for rates is currently downwards.

- But 1.5 million homeowners will come to the end of their fixed-rate mortgage deals in 2024 and at the moment there still remains a wide gulf between the interest rates on new lending (gross advances) and existing lending (balances outstanding).

- On latest data shows the average fixed rate for new lending was 4.73% whilst the average for existing borrowers was 2.76% (data to end Q3).

- These borrowers will almost certainly face an uplift in their monthly mortgage costs but it is worth shopping around for deals because, unless there is a dramatic change, swap rates and mortgage rates are on a downward trend.

The Good News

- Many big mortgage lenders are in fierce competition and slashing rates. The average five-year fix is now 5.55%, down from its peak of 6.37% in August, while the two-year stands at 5.93%, down from 6.86% in July.

- Santander and HSBC are the latest to join the sub 4% club for a five-year fix, whilst Barclays have unveiled two-year deals within touching distance of the 4% threshold.

- Product choice rose for the sixth month in a row, reaching 5,899 options, a 15-year high. The average shelf life of a product has lengthened to 21 days, the highest level since June, indicating increasing stability in the market.

- Forecasters at three leading institutions suggest the inflation rate will halve to 2% by April, potentially meaning the Bank of England could bring forward the date of its first interest rate cut.

Source: Dataloft, Investing.com, Bank of England, FCA, Moneyfacts, Oxford Economics, Investec, Deutsche Bank, Santander, HSBC and Barclays, subject to conditions, fees and loan-to-value

If you need help with this. Please get in touch with us. We’re happy to help.

Jamie